Giving money to loved ones can help with education, housing, or other big life expenses. But before you write that check, you should know the tax rules and regulations—especially in the US.

Here’s a rundown of the annual gift tax exclusion limits, lifetime exemptions, and best practices to stay within the lines.

What is a gift?

Any time you transfer an asset—cash, property, or other valuables—to someone else without full compensation, it’s a gift.

Examples:

Giving a check to a family member.

Paying someone’s tuition or medical bills for them.

Transferring property ownership (e.g., a house or car) without full payment.

What is the gift tax?

The gift tax is a federal tax in the US imposed on transferring money or property to another person when the giver (donor) doesn’t get something of equal value in return.

While this tax is technically the donor’s responsibility, in practice, most Americans never owe gift tax because of the IRS’s gift tax exemptions and exclusions.

The gift recipient does not need to pay income tax on the gift, but there are considerations related to capital gains tax when gifted securities are sold.

What is the gift tax return?

If you make a taxable gift, you must file Form 709: U.S. Gift (and Generation-Skipping Transfer) Tax Return.

The gift tax return is due April 15 of the following year or the next business day if it falls on a weekend or holiday.

You should complete Form 709 anytime you gift more than the annual exclusion amount.

What is the Annual Gift Exclusion?

The annual exclusion lets you give up to a certain amount each calendar year to anyone without reporting the gifts or using up your lifetime exemption.

Here are the annual gift exclusion limits per person for the last two years:

2023 annual gift exclusion: $17,000 per person.

2024 annual gift exclusion: $18,000 per person (adjusted for inflation).

So, in 2024, you can give up to $18,000 to each family member (or anyone) without those gifts counting against your lifetime gift exemption or requiring you to file a gift tax return.

If you are married, you and your spouse can give up to $18,000 each to the same person—$36,000 total—without having to file a gift tax return.

If you give more than the annual exclusion to any one person in a tax year, the overage will count against your lifetime exemption, but you won’t owe any tax until you exceed that lifetime limit.

What is the Lifetime Estate and Gift Tax Exemption?

The lifetime estate and gift tax exemption is the total amount of gifts and estate value you can transfer over your lifetime (and upon death) without triggering federal gift or estate tax liability.

2023 Lifetime Estate and Gift Tax Exemption: $12.92 million per individual.

2024 Lifetime Estate and Gift Tax Exemption: $13.61 million per individual (estimated based on IRS inflation adjustments).

If, throughout your lifetime, you give away more than these amounts in combined gifts and estate transfers, you (or your estate) would likely owe a federal gift tax return due on the excess. Most people never exceed this limit, so most Americans are unaffected by federal gift tax.

Are there any special rules and exceptions?

There are some special rules and exceptions.

1. Spouse Exemption Gifts to a U.S. citizen spouse are unlimited and do not count towards the annual exclusion or lifetime exemption. There is a yearly limit if your spouse is not a U.S. citizen.

2. Education and Medical Expenses Payments made directly to an educational institution for tuition or directly to a medical provider for someone else’s qualifying medical expenses are generally not gift tax rules.

If you pay the institution or provider directly, these payments do not count towards your annual or lifetime exemption amounts.

3. Gift splitting married couples can gift split. This means any gift made by one spouse can be treated as if both spouses made it. This allows couples to combine their annual exclusions (e.g., double from $18,000 to $36,000 per person in 2024) without using their lifetime exemption.

4. With State Gift Taxes, most U.S. states do not have a gift tax. However, some states have their own estate or inheritance tax. Check your state’s laws.

What is Fair Market Value?

When gifting assets, you need to know the asset's fair market value (FMV).

FMV is the price a buyer would pay for the asset in an open market. This is important for gift tax purposes. The IRS requires you to report the FMV of the gifted asset on the gift tax return (Form 709) so you can calculate the gift tax correctly.

For instance, if you gift your child a piece of real estate, the FMV would be the current market value, not the original purchase price. If the property appreciates since the original purchase, the difference would be a taxable gift.

You should consult a tax professional or appraiser to determine the FMV of the asset being gifted. This will ensure the gift tax return is accurate and complete so you don’t get hit with penalties or audits.

What should you consider when giving real estate?

Giving real estate is more than just signing a deed – it has financial and tax implications that need to be considered.

One strategy is to use a trust which will protect the property and the beneficiary’s long term interests.

Also, transferring real estate to family members through gifting will reduce the size of your estate and potentially lower estate tax.

As with any big financial decision, consult a professional to make sure your plan is current and fits your overall estate goals.

How does gifting to minors and grandchildren work?

Gifting to minors and grandchildren can be a great way to fund their future, but you must consider the tax implications and consequences.

Gifting to minors

Consider the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA) custodial accounts when gifting to minors.

These accounts allow you to transfer assets to a minor, but the minor does not have control over the assets until they reach the age of 18-25 years old, depending on the state.

The benefits of UTMA/UGMA accounts include:

Tax benefits: The income earned on the assets in the account is taxed at the minor’s tax rate, typically lower than the adult’s tax rate.

Simplified management: The account is managed by an adult (the custodian) until the minor reaches the age of majority.

However, there are also potential drawbacks to consider:

Loss of control: Once the minor reaches the age limit, they gain control over the assets, and you may not have any say in how the assets are used.

Tax implications: The assets in the account are considered the minor’s assets, and the income earned on the assets may be subject to the “kiddie tax” (tax on unearned income of minors).

Gifting to grandkids

Gifting to grandkids can help with their education or other expenses. One way to do that is to contribute to a 529 college savings plan.

These plans offer:

Tax free growth: The investments grow tax free.

Tax free withdrawals: Withdrawals are tax free if used for qualified education expenses.

You can also gift to a trust which gives you more control over the assets and how they are used.

State gift tax rules

Federal gift tax applies to all states but some states have their own gift tax and exemption rules. Know the state rules to be compliant and tax efficient.

Some states have a state gift tax, while others do not.

For example:

States with gift tax: Connecticut, Delaware, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Vermont, and Washington have a state gift tax.

States without gift tax: Other states, such as California, Florida, and Texas, do not have a state gift tax.

It’s essential to consult with a tax professional to understand the state-specific gift tax laws and exemptions that apply to your situation.

How can Shoeboxed help when gifting money to family members?

Giving money to family members can be a great way to support their financial goals—tuition, medical expenses, or a holiday surprise.

There are many tax rules and regulations to consider (annual exclusions, lifetime exemptions, and reporting requirements), but staying organized and documenting your gifts is one of the most important parts.

This is where Shoeboxed can really help.

1. Centralized recordkeeping

When gifting money, you’ll want to keep track of:

Dates and amounts of each gift

Recipients (especially when making multiple gifts in a single year)

Proof of payment or related receipts

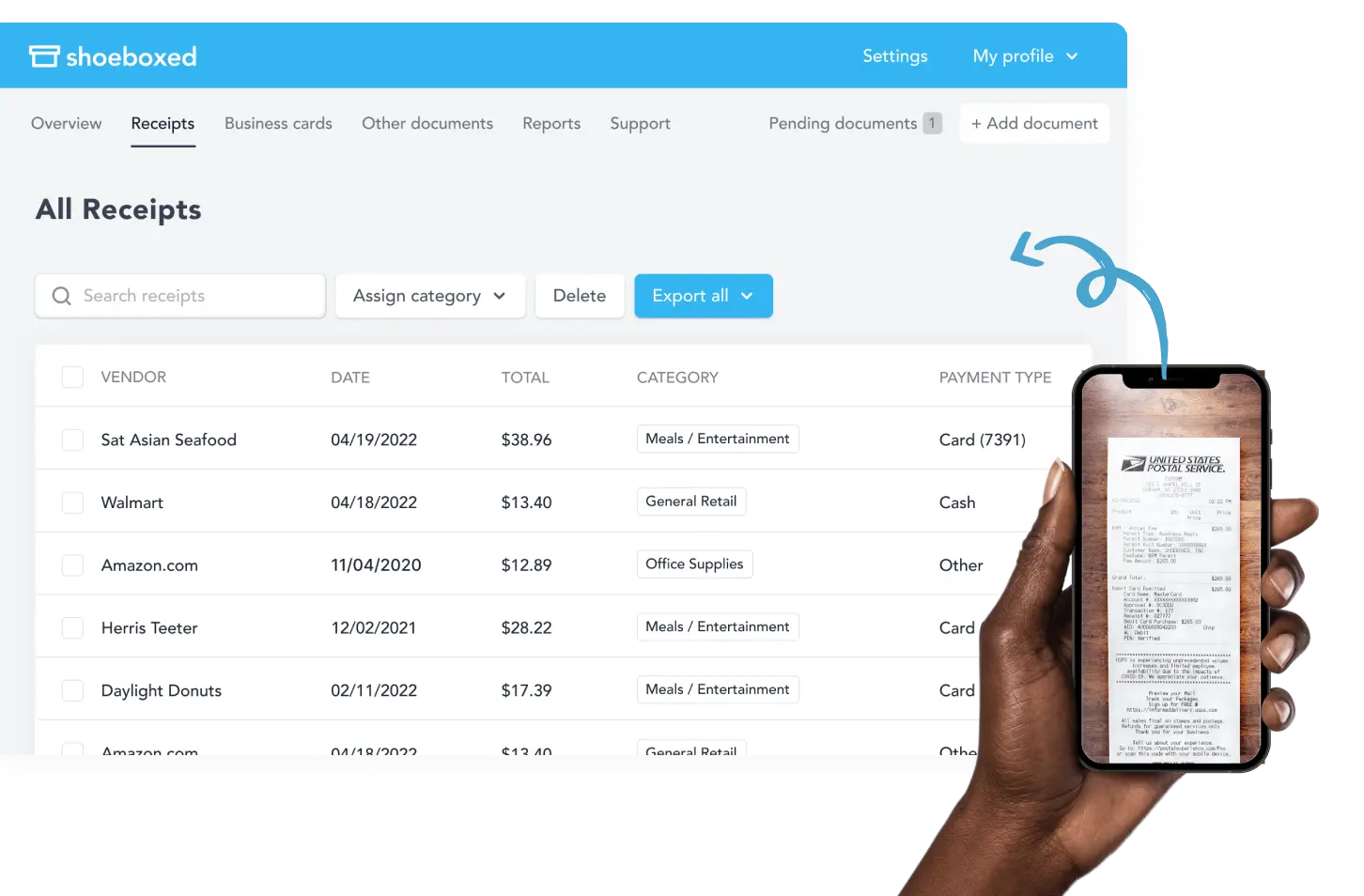

Shoeboxed allows you to upload, scan, and store receipts and financial documents in one central, cloud-based location. If you write a check, for example, you can scan or snap a photo of the check stub or the bank statement and upload it into Shoeboxed. That way you’ll have a permanent, easily accessible record of each gift.

To do this, simply snap a picture of your receipt with your smartphone and Shoeboxed's app will automatically upload it to your designated account.

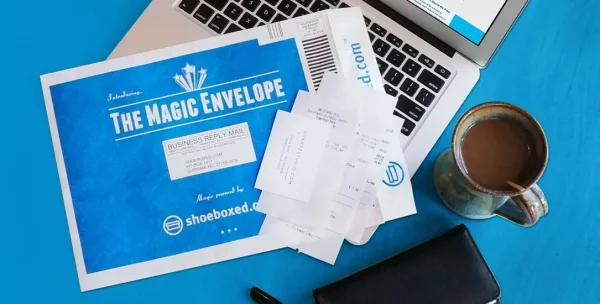

Suppose you have a stack of paper receipts. Shoeboxed even offers a mail-in service (the “Magic Envelope”) where they’ll scan, categorize, and upload everything for you, creating a digital copy of your receipts.

Having accurate and easily accessible records makes it easier to:

Verify the total amount given to each recipient for the annual gift tax exclusion.

Track your gifts against your lifetime estate and gift tax exemption.

Provide documentation if the IRS ever asks for proof of gifts

Shoeboxed is the only receipt scanner app that will handle both your paper receipts and your digital receipts—saving customers up to 9.2 hours per week from manual data entry!

Stop doing manual data entry 🛑

Outsource receipt scanning to Shoeboxed’s scanning service and free up your time for good. Try free for 30 days!✨

Get Started Today2. Categorization and organization

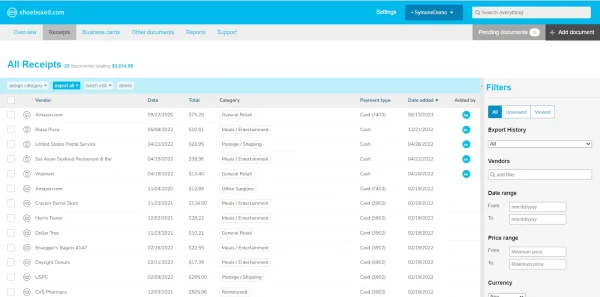

Once you upload documents to Shoeboxed (via mail-in service, mobile app, or web upload), you can categorize your records with custom labels and folders. For example, you might create a folder or tag like “Gifts to Family 2024” to keep all related documents together.

Shoeboxed will automatically scan receipts, extract receipt information (vendor, date, total amount), and categorize the expense for you.

Automatic categorization allows for:

Quick sorting: Find gift-related records among your other financial documents.

Filing ease: If you must file a gift tax return (Form 709), you can quickly retrieve all gifts above the annual exclusion threshold.

Year-to-year comparison: Compare gifts from one year to another without digging through stacks of paper.

3. Tracking expenses for educational or medical gifts

One way to avoid having a gift count towards your annual or lifetime exemption is to pay qualified educational or medical expenses directly to the institution or provider. While these direct payments are not considered taxable gifts, documentation is still essential.

You can:

Store tuition invoices or medical bills you’ve paid on behalf of your family members.

Keep proof of direct payments to schools or healthcare providers.

If the IRS ever asks questions, you’ll have timely and accurate documentation showing that the payment was made directly to the institution, not to the individual.

In the event of an audit, you’ll be able to prove the nature of these excluded gifts.

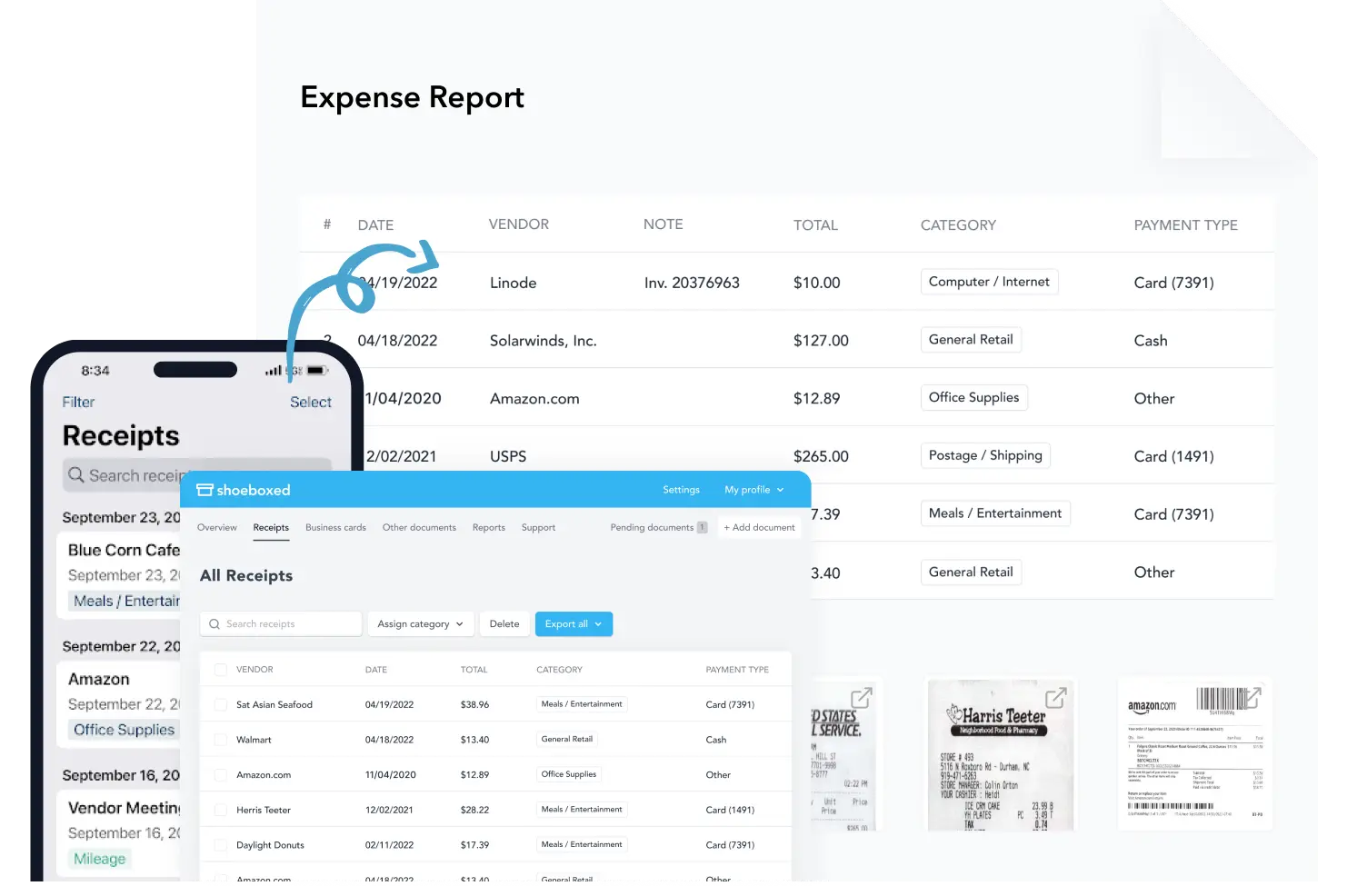

4. Expense reports

Shoeboxed allows you to generate expense reports with receipts attached based on your uploaded documents. These reports can be exported in various formats (PDF, CSV, etc.).

This helps with:

Gift totals: Compile a report of all gift-related transactions for any period.

Professional documentation: Ready for tax professionals or financial planners.

Budgeting: If you have an annual or monthly budget for gifts, Shoeboxed’s reports will help you see how you’re spending vs your plan.

5. Working with tax professionals

If you work with a CPA, financial planner, or tax attorney, giving them direct access to your Shoeboxed account (or exporting specific files for them) makes data sharing a breeze.

Your advisor can review receipts and gift amounts in real-time, give you more accurate guidance, and make sure you comply with the IRS.

Using Shoeboxed when working with tax professionals results in:

Fewer mistakes: Reduces the chance of missing a gift or misreporting the amount.

Time saver: Eliminates back-and-forth emails or physical mail of paperwork.

More accurate advice: With all your financial documents at your fingertips, advisors can tailor their advice to your situation.

Having all your gift documents in Shoeboxed lets you or your tax professional see the total gifts and what needs to be reported.

Turn receipts into data with Shoeboxed ✨

Try a systematic approach to receipt categories for tax time. Try free for 30 days!

Get Started TodayFiling a gift tax return

Even if no gift tax will be owed, you may need to file a gift tax return (IRS Form 709) in certain situations:

If you give more than the annual exclusion amount ($18,000 in 2024) to any single recipient within the same calendar year.

If you and your spouse choose gift splitting.

If you have a future interest in the property (e.g., placing assets in a trust where the beneficiary doesn’t have immediate ownership).

Filing Form 709 does not automatically mean you owe taxes; it simply keeps track of amounts that exceed the annual tax exclusion and counts them against your lifetime estate tax exemption amount.

Best practices for giving money to family

I have found these five suggestions to be some of the best practices to follow when gifting money to a family.

1. Stay under the annual exclusion

To avoid paperwork and avoid using up your lifetime exemption, try to keep individual gifts under the annual exclusion per person.

2. Use direct payments for medical or educational expenses

Pay the provider directly if you want to pay for tuition or medical bills. This way, you can avoid gift tax rules on those amounts altogether.

3. Keep records

Document all gifts, including dates, amounts, and any conditions. If you file a gift tax return (Form 709), keep copies for your records.

4. Trusts for bigger gifts

If you transfer a lot of wealth, a trust can offer tax benefits and control over how and when your family members get the money.

5. Get a pro

Tax laws change, and your situation is unique. A tax attorney or CPA can advise you on your situation and keep you in compliance with the changing rules and tax consequences.

What are some common misconceptions?

Here are three of the most common misconceptions that I have encountered.

1. “The recipient pays the gift tax.”

False. The donor (giver) of financial gifts is generally responsible for any potential gift tax.

2. “All gifts above the annual exclusion are taxable.”

Not necessarily. Only if you exceed your lifetime exemption might you owe tax.

3. “I don’t need to file a return if I exceeded the limit but didn’t exceed the lifetime exemption.”

You do need to file Form 709 if your gift to an individual goes over the annual exclusion in a single year, even though you may not owe taxes.

Seeking professional advice

Gifting large amounts of money or assets to family members can become complicated from a tax and financial planning perspective.

A certified professional accountant (CPA) or other tax professional can help walk you through potential tax implications for your gifts and how to handle them.

A financial professional can help you consider how making a gift to family members will impact your own finances.

Frequently asked questions

Do I have to pay taxes if I give money to my family?

In the US, most people don’t have to pay gift tax because of two big exceptions:

Annual Gift Tax Exclusion: In 2024, you can give up to $18,000 per person per year and not use up your lifetime exemption. You also don’t have to file a gift tax return for amounts under this threshold.

Lifetime Estate and Gift Tax Exemption: If the gift is over the annual exclusion, you’ll have to file a gift tax return (Form 709), but you usually won’t have to pay taxes unless your total gifts over your lifetime exceed the multi-million dollar lifetime exemption ($13.61 million in 2024).

So, for most people, gifting money to family won’t trigger a tax.

Do I have to file a gift tax return for every gift above the annual exclusion amount?

If you exceed the annual exclusion amount to anyone in a calendar year, you must file a gift tax return (Form 709). But filing Form 709 doesn’t mean you owe taxes. It just tracks the amount you have given.

You only start to owe gift tax if your total gifts exceed that big lifetime limit.

Some gifts—tuition or medical expenses—are not subject to gift tax if you pay the institution or provider directly.

In conclusion

Giving money to family members can be a loving act and a way to pass on financial support. For most people, the interplay of the lifetime estate and gift tax exemption and annual gift tax exclusion means that actual gift tax exposure is minimal.

However, using Shoeboxed to track and store documentation for these gifts and consulting a tax professional will ensure you meet all of the IRS's regulations and tax laws.

Caryl Ramsey has years of experience assisting in bookkeeping, taxes, and customer service. She uses various accounting software to set up client information, reconcile accounts, code expenses, run financial reports, and prepare tax returns. She is also experienced in setting up corporations with the State Corporation Commission and the IRS and is a contributing writer to SUCCESS magazine.

About Shoeboxed!

Shoeboxed is a receipt scanning service with receipt management software that supports multiple methods for receipt capture: send, scan, upload, forward, and more!

You can stuff your receipts into one of our Magic Envelopes (prepaid postage within the US). Use our receipt tracker + receipt scanner app (iPhone, iPad, and Android) to snap a picture while on the go. Auto-import receipts from Gmail. Or forward a receipt to your designated Shoeboxed email address.

Turn your receipts into data and deductibles with our expense reports that include IRS-accepted receipt images.

Join over 1 million businesses scanning & organizing receipts, creating expense reports and more—with Shoeboxed.

Try Shoeboxed today!